For years, Cook Islanders have been told that the minerals on our seabed will make our nation rich. But a growing body of independent evidence shows that deep seabed mining is not the economic miracle, as it has been sold to us. It is a high-risk, high-cost industry built on speculation and unproven technology with promises of economic wealth that have yet to be proven.

A 2025 assessment by Michael Barnard and Lyle Trytten found that the seabed mining industry is built on overly optimistic assumptions. According to the report, companies are underestimating costs and relying on technology that has not been proven to work at full scale in the deep ocean. This means the industry is likely to be far more expensive and far less profitable than people have been led to believe.

This is important because the Seabed Minerals Authority (SBMA) and the mining companies are telling the public that Cook Islands nodules are “more likely than not” to be economically viable. Yet SBMA also admits there are no advanced studies yet for Cook Islands high-cobalt nodules on their actual worth due to fluctuations in the market, and that a proper study on production costs is still needed.

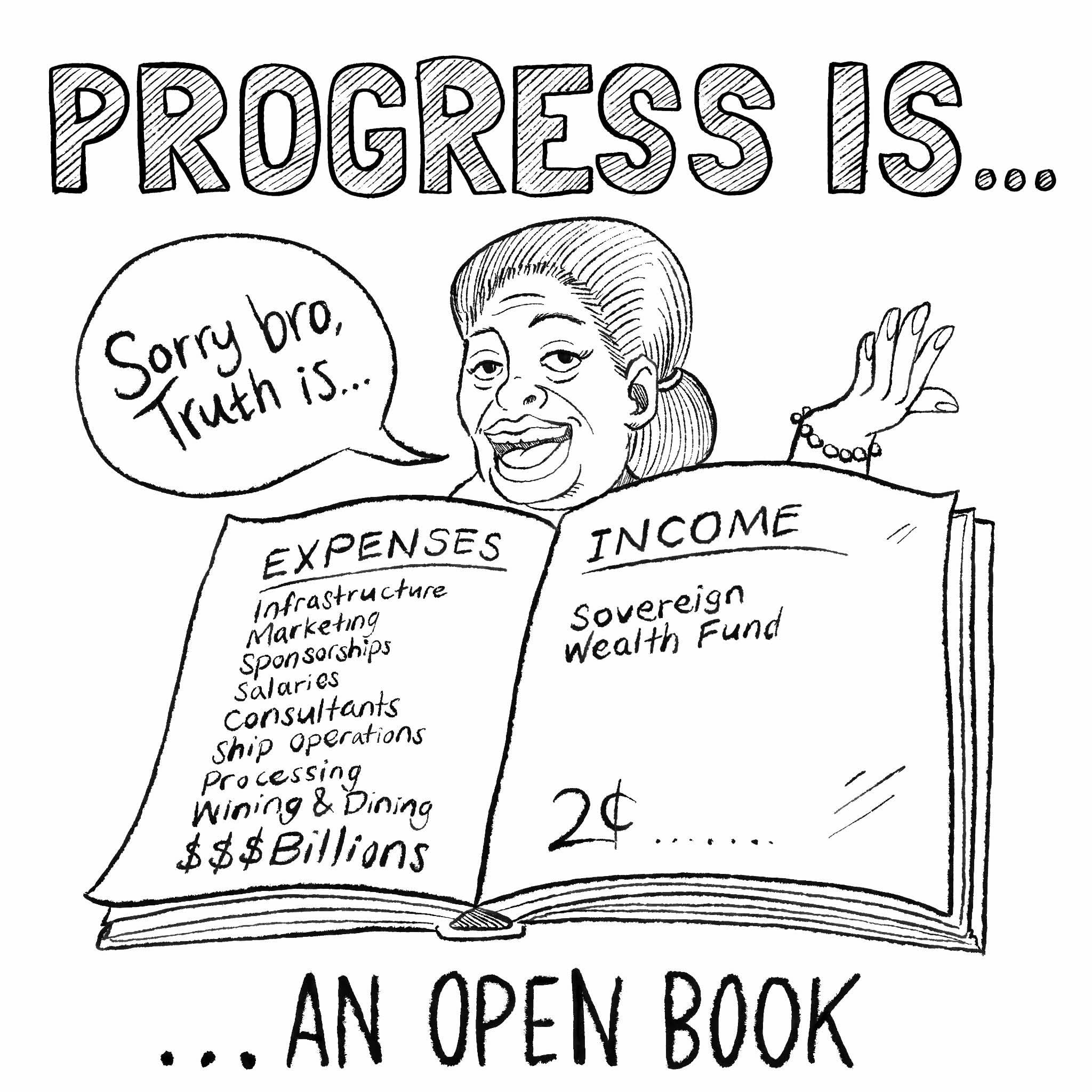

Independent analysis by Greenpeace found that the nodules may be worth only US$100–140 per dry tonne on the open market, while estimated costs to extract a tonne of nodules are around US$200, or higher. That means the project is already underwater before transport, processing, financing, rehabilitation, or cost overruns are fully taken into account. When recovery costs are higher than the value of the nodules once sold, this is not a pathway to prosperity, it is a pathway to loss.

Other recent analysis raises more red flags. This year a review of The Metals Company’s pre-feasibility study by Steven H. Emerman identified serious gaps. This assessment pointed to the lack of a proper waste management plan, unanswered questions about potentially toxic by-products, and inconsistencies in the company’s resource figures. If a major seabed mining company cannot yet show a solid business plan on paper, the public has every reason to be cautious about promises of wealth.

The deeper problem is that the economics of seabed mining often focus on hoped-for revenues, while downplaying the true costs. In 2023, renowned economist Professor Rashid Sumaila and his co-authors concluded that once the full net costs of deep seabed mining are taken into account, the industry is unlikely to be attractive to most stakeholders. A recent economic analysis estimated that while deep seabed mining could generate around US$12 billion globally in direct financial gains over 50 years, the non-financial costs of damage to ocean ecosystem services, including carbon storage, climate regulation and biodiversity support, could total US$68 billion to US$105 billion, meaning society could lose US$5.60 to US$8.70 for every US$1 gained. That same analysis found the economics are extremely fragile: a 42% drop in mineral prices or an 85% cost overrun would wipe out all projected financial gains. In fact, the authors concluded that even if the cost of extracting minerals from the seabed were reduced to zero, the overall net value would still be negative once the wider losses to the ecosystem were included. A separate study by Planet Tracker has warned that the total value destruction from harm to these ecosystem services could exceed US$500 billion.

We have already seen Deep seabed mining lose support from both buyers and backers. Major companies including Google, BMW, Volvo Group and Samsung SDI have publicly committed not to source seabed minerals, excluding them from their supply chains. That trend reflects a broader shift toward tighter ethical sourcing standards, with companies such as OnePlus also publishing policies to avoid minerals linked to conflict and armed groups.

That opposition is also growing across the finance sector. UNEP Finance Initiative has said there is “no foreseeable way” that financing deep-sea mining, in its current form, can be considered consistent with Sustainable Blue Economy Finance Principles, while a 2026 report by Seas At Risk and the Deep Sea Mining Campaign found that 82 financial institutions representing around €24 trillion in assets now exclude, restrict or have publicly raised concerns about investing in the industry.

If deep seabed mining proceeds, there is no credible evidence that the people of the Cook Islands will receive a major financial windfall. In 2023, Wilde and colleagues found that direct payments to states would likely be economically insignificant. Jaeckel and van Doorn pointed out in 2025 that mining in international waters cannot legally move ahead without separate benefit-sharing rules, and those rules are still far from complete. Pickens and co-authors also identified in 2024 more than 30 major unresolved issues in the draft international deep-sea mining regulations, showing just how uncertain and incomplete the governance framework remains at an international level. Meanwhile, the Cook Islands Government apparently knows better and has already passed our deep seabed mining regulations. That does not mean mining has been approved here, it has not, but it does show how quickly the legal machinery is being built around an industry whose global rules, benefit-sharing system, and economic case are still unresolved.

The people of the Cook Islands deserve honesty, not hype. The evidence increasingly shows that deep seabed mining is not a guaranteed path to prosperity, but a high-risk bet with uncertain returns and likely very real long-term costs. If the costs outweigh the profits, who really stands to benefit, and who gets left to deal with the environmental fallout?

Our ocean and livelihoods are our permanent heritage, not commodities or an inventory of resources to be traded for unsure market gains, or even worse, losses!